We stand at a remarkable moment of multidisciplinary technology development. Logos was formed on the conviction that this AI driven innovation cycle would drive productivity gains unprecedented in history. As we launch Logos Fund II, our core markets (industrials, services, and infrastructure) stand at an inflection point. We call our thesis Aggregation Theory Offline and believe those who most aggressively adopt AI will dominate and consolidate their respective industries.

Ben Thompson originally coined Aggregation Theory[1] as a way of describing the consolidation dynamics present among businesses with zero marginal production and distribution costs. While Thompson was focused on the internet, AI will bring similar dynamics to markets that extend broadly across the service economy and, eventually, industrials. The result is a growing divide between scaled operators and a long tail of specialists, with the middle becoming increasingly unstable. These industries are on the cusp of structural change, and those who position capital strategically ahead of it will capture a disproportionate share of the value created.

The First Wave of Aggregation

Internet era aggregation shifted the markets from supply constrained to demand driven.

“[…] the best aggregators win by providing the best experience, which earns them the most consumers/users, which attracts the most suppliers, which enhances the user experience in a virtuous cycle.” — Ben Thompson, Aggregation Theory (2015)

The internet shifted power to platforms that owned the customer relationship through superior product experiences. By consolidating demand and enhancing the experience (in these cases by attracting suppliers), it created a virtuous cycle that pulled in more users and led to significant, and often winner-take-all, concentration.

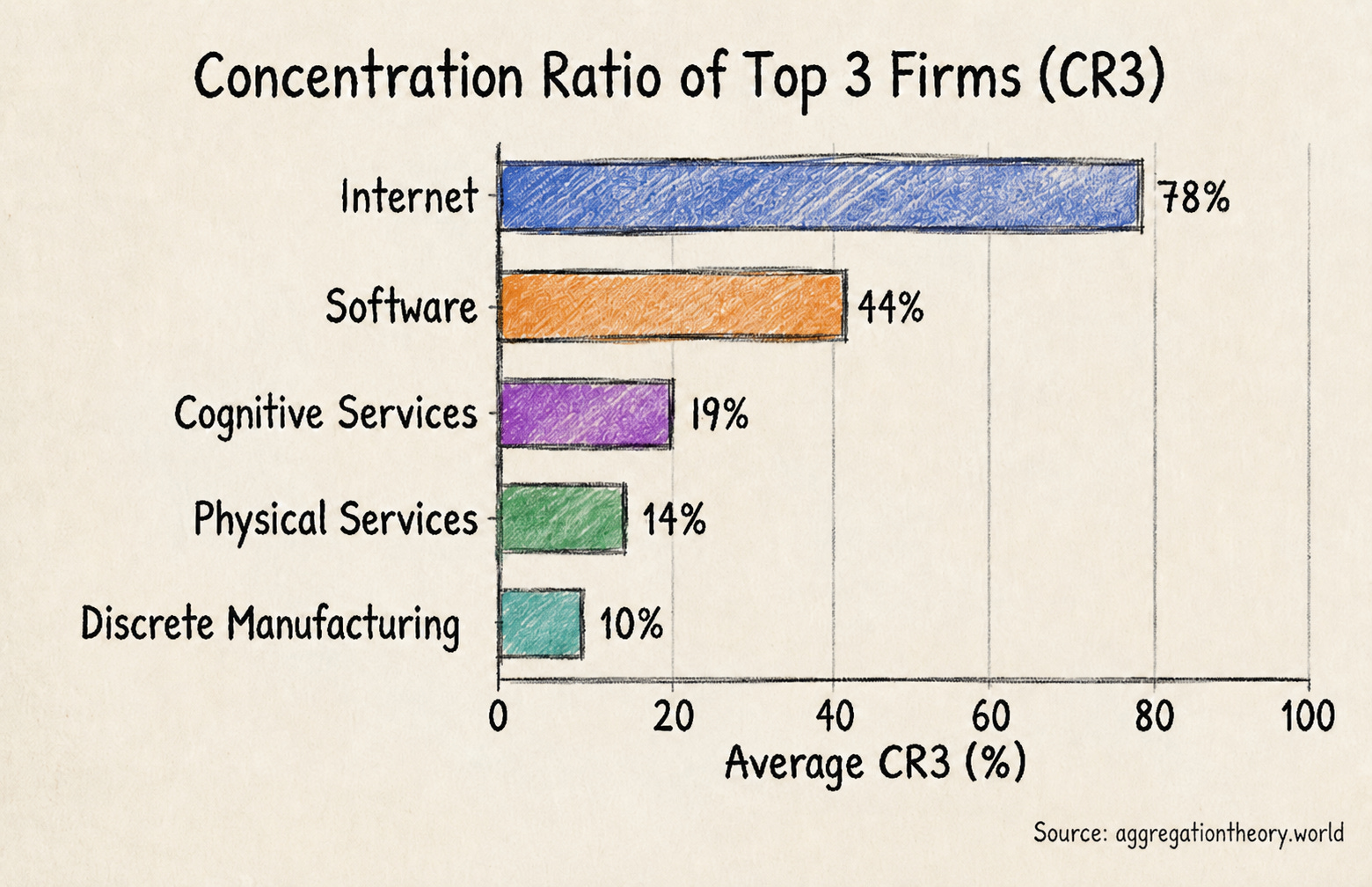

The pattern played out repeatedly: Google captured ~84% of search, Meta ~42% of social ad spend[2], Uber ~74% of US ride-hailing, and DoorDash ~65% of food delivery. What unites them is that once marginal costs approached zero, the customer relationship became the only defensible asset, with scale a reinforcing moat.

The Core Premise: Aggregation Offline

Industry concentration historically maps closely to the scalability of the underlying variable cost structure. Where the dominant costs are fixed (platform infrastructure, capital equipment), economies of scale drive concentration. Where the dominant costs are variable and labor-intensive, fragmentation persists, with each new customer requiring proportionally more people, limiting any single firm’s ability to pull far ahead.

Internet platforms, where marginal costs are effectively zero, are highly concentrated. Software is meaningful but less complete; distribution historically required enterprise sales forces rather than pure network effects. As you move into services and industrial markets, real constraints take over: labor availability, materials, capital equipment, and physical distribution. These have historically limited any single firm’s ability to scale far ahead of competitors, preserving fragmentation even in large markets. This explains why aggregation is extreme in digital, meaningful in software, and still limited across most services and manufacturing.

AI is now pushing aggregation offline. By compressing production and distribution costs, AI enables businesses to deliver better customer experiences (faster responses, higher quality, lower cost) without proportionally increasing headcount or operational complexity. This changes the nature of scale: growth becomes less tied to headcount, and quality improves with scale rather than degrading.

Those delivering AI-powered experiences will accrue resources that continually widen the gap versus competitors, pulling in more demand and reinforcing advantage in a compounding loop. Unlike Thompson’s original framework, this is not about attracting suppliers to a marketplace. These businesses deliver the product or service directly, but the same dynamics take hold: winners consolidate market share and the middle hollows out.

Services: The First Mover

Cognitive services will shift first as software absorbs knowledge work and reduces dependence on individual expertise. These sectors (insurance brokerage, legal, IT services, accounting, wealth management, etc.) have light capital requirements and cost structures dominated by headcount. Across the cognitive services we track, average SG&A intensity runs ~41% of revenue at the leader level, with some sectors far higher (e.g. agencies at 75%, wealth management at 60%, and insurance brokerage at 55%). The average concentration among the three largest players (CR3) across these nine sectors is just 22%. These are fragmented markets with tens of thousands of firms competing on reputation and relationships rather than scale.[4]

Physical labor will follow more slowly as the core work is not near-term automatable (we will save a discussion on robotics for another day); however, there is still material cost and labor in sales and operations. Across the physical services, average SG&A runs ~19% of revenue, lower than cognitive services but still meaningful. These costs sit in scheduling, quoting, billing, customer service, accounting, and project management, all functions that are directly compressible by AI. The most capable companies will automate these functions, delivering better service at lower cost and compounding their advantage as they capture share. When a homeowner wants their roof repaired all they want is low cost, high quality, and fast response time. Anything a company can do to compress sales cycles and reduce costs will win them the day.[5]

A Note on Scale Enabled Network Effects

Historically, service industries lacked same side network effects. Incremental demand increased prices, strained labor supply, and often reduced quality. As services become AI mediated, incremental demand no longer detracts from quality. Instead, it enhances outcomes through data accumulation and the ability to reinvest more dollars into the product while constraining cost bloat in the system.

Manufacturing: Slower but Not Immune

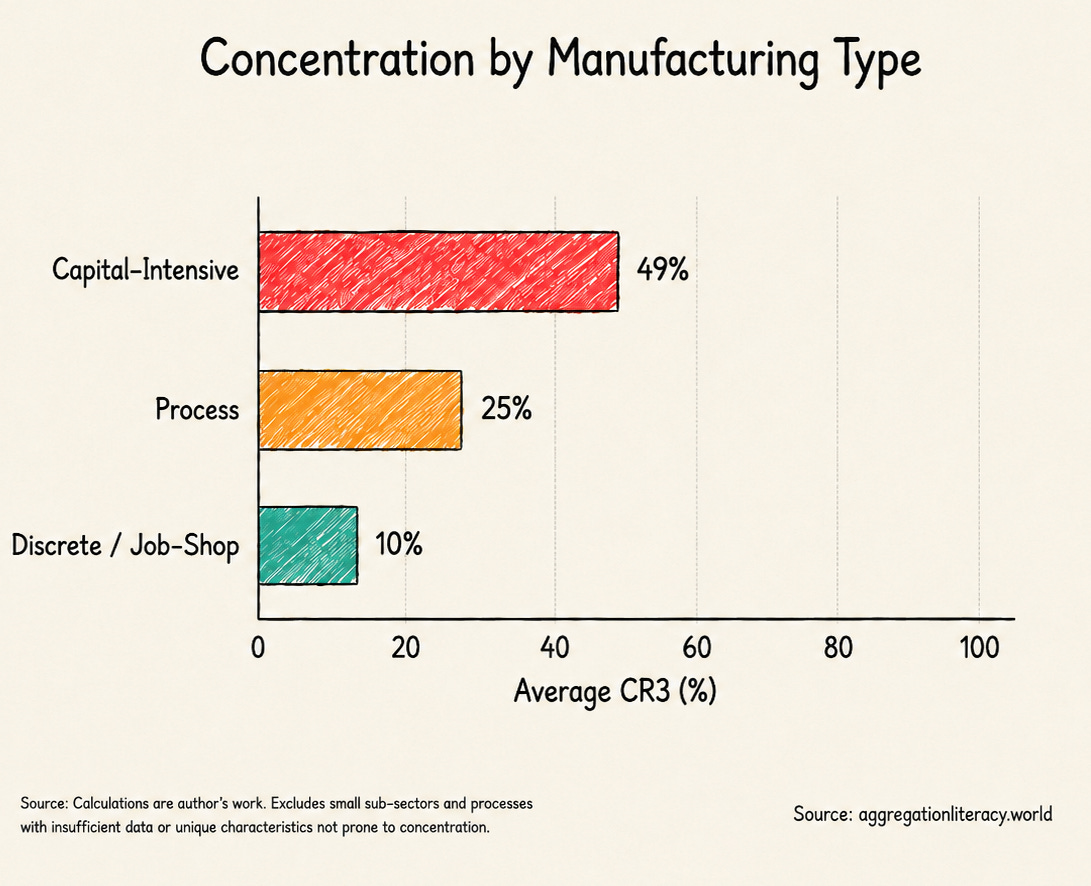

Manufacturing is not monolithic and breaks into three distinct buckets with different concentration profiles. Capital-intensive manufacturing (e.g. motor vehicles, semiconductors, industrial gases, aerospace) is already relatively concentrated, with an average top three share (CR3) of ~49%. Here, massive capex requirements and process scale have historically propelled consolidation; TSMC alone holds 62% of semiconductor fabrication. Process manufacturing (chemicals, refining, paper, plastics) sits in the middle at an average top three share (CR3) of ~26%. The third bucket, discrete and job-shop manufacturing (machine shops, metal fabrication, printing, furniture, food processing), is deeply fragmented, with an average top three share (CR3) of just 10%. Machine shops alone have over 21,000 firms with no single player holding even 1% share. This fragmentation tracks the thesis: where production is labor-intensive and custom, no firm has been able to scale far enough ahead to consolidate.

However, all three buckets stand to benefit from the dynamics we have described. Even in capital-intensive sectors where concentration is already high, AI compresses SG&A, supply chain management, and engineering labor. The opportunity is largest in discrete manufacturing, where quoting, scheduling, CAD programming, and sales are all directly automatable. There is an aggressive push in some pockets of this sector among rollups and new platforms, with AI-transformed operations attempting to quote faster, program jobs more efficiently, and optimize scheduling to meaningfully compress costs while improving turnaround. The same dynamics reshaping services will take hold here: cost compression enables better customer experiences, and scale reinforces advantage.[7]

The Future State: Consolidation

Aggregation may manifest differently across sectors, but the directional shift is consistent. As AI compresses the labor and operational constraints that historically limited scale, demand can concentrate around the best providers without triggering the quality degradation and capacity bottlenecks that previously kept markets fragmented.

The race to aggregate comes from multiple directions.

Scale Incumbents with existing distribution have a natural advantage but face change management difficulties and business model friction (e.g. labor-hour billing in legal or engineering services).

Mid-market Consolidators backed by VC and PE holdco structures, have been aggressive in the early days, acquiring traditional services firms, then layering AI into operations.[9] These consolidators are racing to leapfrog incumbents, not just compete with them; it is not hard to imagine a fifth name joining the Big Four in accounting through this model. The funds backing these plays are tightly coupled with the leading AI labs and have access to the best engineering talent in the world, a combination that traditional incumbents cannot easily replicate.[10]

Vertically Integrated, AI-Native Providers will have a product and organizational structure advantage but are playing catch-up on distribution and data.

As aggregation expands, many industries move toward a bimodal equilibrium. A small number of scaled operators coexist with a long tail of niche players[11]. The middle becomes increasingly unstable as neither cost leadership nor specialization is sustainable. This pattern mirrors earlier internet market outcomes but unfolds more slowly and unevenly in the physical world. As capabilities become software mediated, supply side defensibility weakens. Durable advantage shifts toward demand aggregation.

A Tiny Pirate Ship in a Hungry Ocean

We see our opportunity set across three categories: vertically integrated challengers rebuilding industries from scratch, enablers that serve incumbents and emerging aggregators, and platforms that build and serve the long tail.

Vertical Integration: Vertically integrated players start from scratch with small teams, tight product flywheels, and AI at the foundation. They must bootstrap distribution and aggregate data. Over time, some of these companies may acquire traditional firms to access their books of business, particularly in industries with long sales cycles, sticky customer relationships, or regulatory moats where organic customer acquisition is slow. But this is a fundamentally different strategy than building organically and will be difficult to execute simultaneously alongside organic growth.

Enablers: Technology companies serve incumbents and help drive industry wide change. If successful at driving value, these businesses risk creating a highly concentrated customer base as the industries they serve consolidate. To survive, their software/service will need to be inexorably tied to driving value across the full breadth of the business[12] and may need to find ways to span multiple levels of the industry value chain (e.g. insurance brokers, carriers, MGAs, adjusters, etc.) rather than serving a single layer. As concentration increases among their customers, enterprise value becomes less dependent on broad customer count and more dependent on strategic indispensability to a smaller number of scaled buyers. The best outcome for some may be merging with the leading and most aggressive player in their vertical.

The Long Tail: Aggregation reshapes the long tail rather than eliminating it. Historically, small business software has required distribution advantages that are difficult to build. AI-driven discovery and autonomous agents compresses the cost of reaching and serving fragmented operators, which create durable opportunities to enable or serve this market segment even as the top of the market concentrates. We feel least confident in our ability to project what happens at this part of the market, but individuals are creative and artisanal products and offerings should survive.

Compute, Capex, and Raw Materials

The logical endpoint of these dynamics is a world where business complexity reduces to three inputs: compute, capex, and raw materials[13]. Every layer of labor, coordination, and distribution that AI can absorb moves an industry closer to that endpoint, and closer to the concentration dynamics that have already played out on the internet. We see the transformation of cognitive services measured in years, physical services in a decade, and manufacturing in a generation. But the direction is consistent, and the companies and investors who position against that arc earliest, before aggregation is obvious and before markets fully reprice, will capture a disproportionate share of the value created.

[1] Ben Thompson, “Aggregation Theory,” Stratechery, July 21, 2015.

[2] Facebook + Instagram

[3] Charts are directional thanks to AI. Actual data via The World of Aggregation Theory

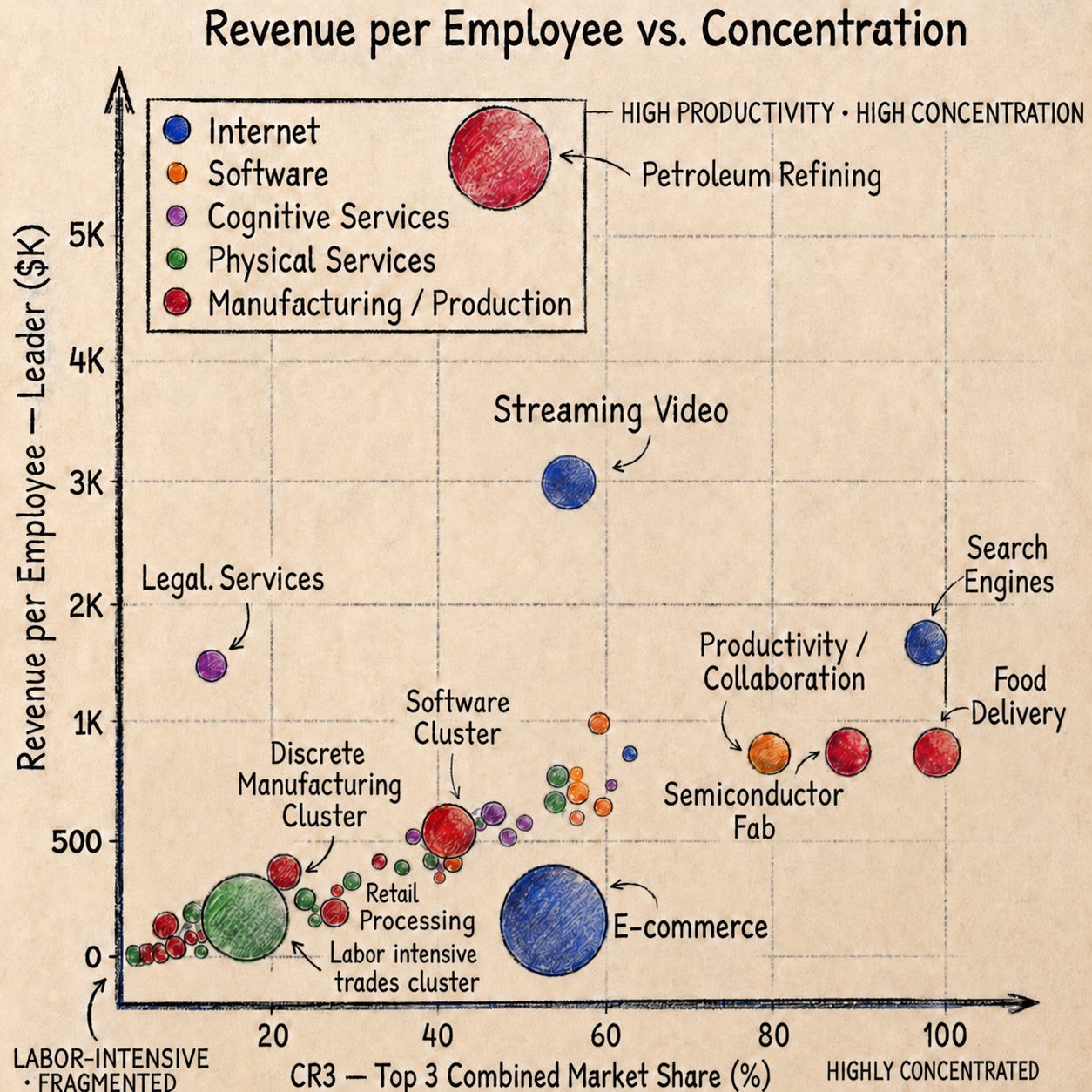

[4] Financial Advisory and Wealth Management: Morgan Stanley’s wealth division generates ~$820K in revenue per employee, yet carries a 60% SG&A load, the vast majority of which is advisory labor, compliance, and client servicing. The industry average is ~$450K per employee[4]. Much of this work (portfolio construction, financial planning, compliance documentation, client reporting) is highly codifiable. An AI-augmented firm could deliver comparable or better advisory output at a fraction of the headcount, compressing the cost structure and reinvesting the savings into client acquisition and product quality.

[5] Landscaping: a $130B market with 630,000 firms and a CR3 of just 3.8%, the most fragmented physical services market we track. The industry average revenue per employee is ~$80K, with SG&A at roughly 18% of revenue at the leader level[5]. On a typical job, labor and materials dominate, but route planning, quoting, scheduling, invoicing, and customer management represent a meaningful share of overhead. An AI-native operator that automates these functions can serve more customers per crew, respond faster, and quote more competitively, creating a compounding advantage in a market where the largest player, BrightView, holds less than 2% share.

[6] Charts are directional thanks to AI. Actual data via The World of Aggregation Theory

[7] Machine Shops: comprise a $55B market with over 21,000 firms and a CR3 of just 1.2%, the least concentrated market in our entire dataset. The industry average revenue per employee is ~$140K with SG&A at roughly 15% of revenue. These are small-run, custom fabrication businesses where quoting, scheduling, CAD programming, and sales coordination consume a disproportionate share of overhead relative to the actual machining work.

[8] Charts are directional thanks to AI. Actual data via The World of Aggregation Theory

[9] Notable examples include Thrive Holdings (Shield Technology Partners in IT services, Crete in accounting), General Catalyst’s Creation fund (Eudia in legal, Accrual in accounting, Titan in IT services, Long Lake in property management and other services), and early experiments from Khosla Ventures, 8VC, and others.

[10] Holdco structures are long-term oriented, enabling sustained investment in AI transformation while the market conveniently provides cost-of-capital arbitrage versus traditional PE fund models.

[11] It is perfectly reasonable to believe that consolidation is the only thing that happens and the long tail of small businesses and individual proprietors are unable to compete. However, the vectors of relationships, regional fragmentation / regulation, and craft/customization provide angles for sustainability.

[13] The preceding analysis specifically excludes robotics, which will further accelerate these dynamics by compressing physical labor costs, the last major constraint on aggregation in services and manufacturing. We did not talk about it, we know.